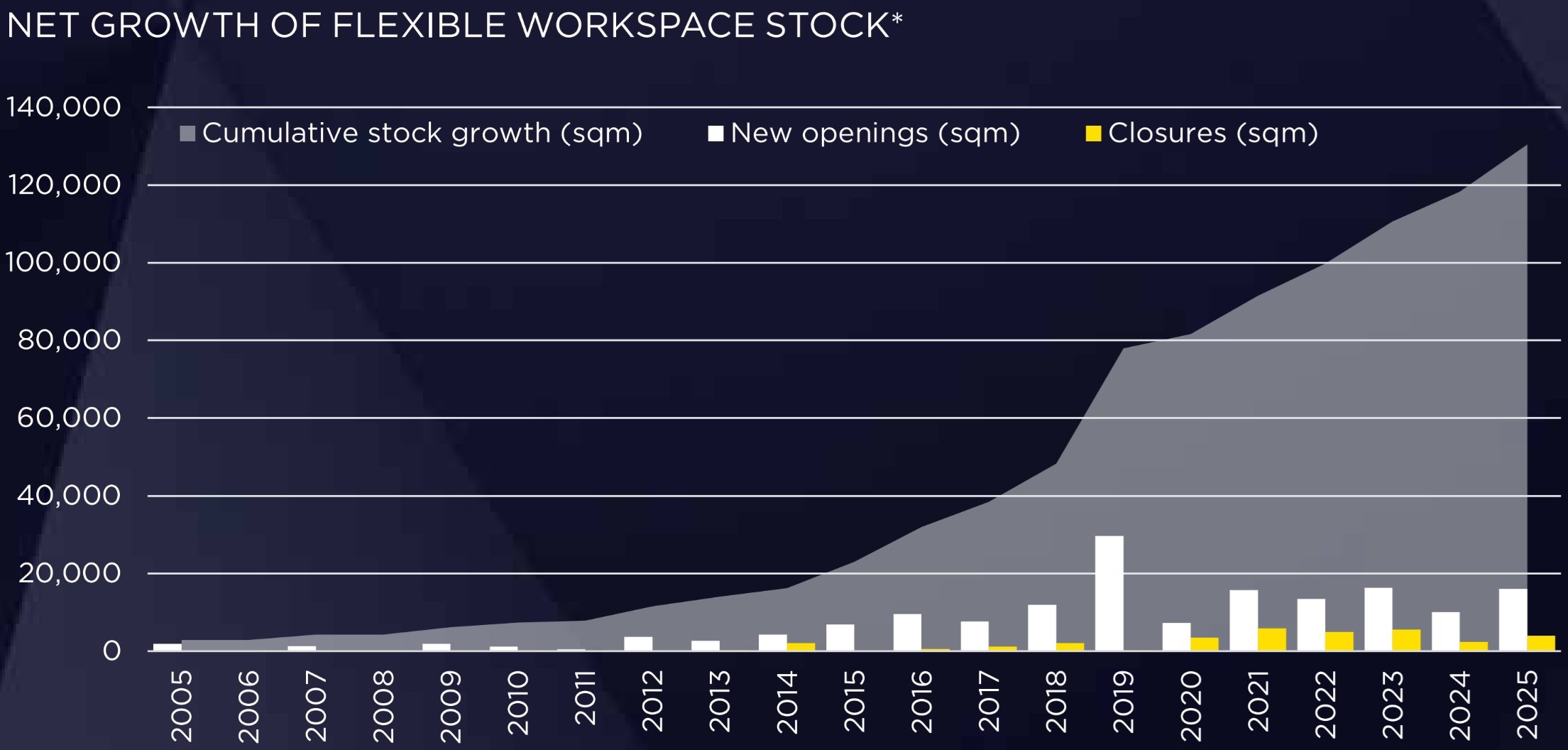

According to the Savills report “Flexible Workspaces in Prague 2026”, the flexible workspace sector has recorded the strongest five-year period in its history. As of December 2025, total flexible workspace stock reached 130,500 sq m, representing a 60 percent increase compared to 2019. The segment, which has been systematically developing in Prague since 2005, has evolved into a fully established and respected segment of the city’s office market, responding to growing occupier demands for flexibility, quality and prime locations.

Historically, 2019 remains the strongest year on record, with nearly 30,000 sqm of new flexible space delivered to the market. This milestone reflected strong pre-pandemic expansion and the entry of new market players, resulting in a 23 percent year-on-year increase in total flexible workspace stock. Although the Covid-19 pandemic in 2020 temporarily slowed growth and led operators to reassess their growth strategies, the sector demonstrated a high degree of resilience and adaptability.

“Since 2021, the market has been gradually stabilising and returning to growth. With 16,400 sqm delivered, 2023 ranked as the second strongest year in the sector’s history, while 2025, with 16,000 sqm of newly opened space, took third place in terms of new supply. The segment clearly confirms its structural growth and its ability to respond to changing workplace models,” says Pavel Novák, Head of Office Agency at Savills.

Strategic tool for companies

“Flexible workspaces are no longer perceived as a short-term solution. They have become a strategic tool for cost and risk management. Companies value the ability to respond flexibly to changes in team size, optimise their real estate portfolios, and operate in high-quality, often premium locations,” adds Pavel Novák.

Demand is being driven by hybrid work models, the growth of outsourcing companies, the expansion of the startup ecosystem and the entry of new firms into the Prague market. A significant driver is also the shift from CAPEX to OPEX, enabling companies to convert upfront capital expenditure into predictable operating costs, thereby increasing financial flexibility and cost transparency.

Market concentration and key players

At the end of 2025, Prague’s flexible workspace market comprised 33 operators across 77 locations. The three largest providers – Scott.Weber Workspace (37 percent), IWG (22 percent) and WorkLounge (12 percent) – control approximately 71 percent of the total flexible workspace stock. While 86 percent of the market continues to be managed by third-party operators, the share of landlord-operated flexible space is steadily increasing. This trend underlines how flexible solutions are becoming an integral part of modern office developments.

Geographical distribution and competition in Prague

The largest volumes of flexible workspace are located in Prague 1 and Prague 4, with nearly 30,000 sqm in each of these districts. Prague 1 hosts nine providers, while Prague 4 accommodates ten operators.

However, 2025 saw the highest increase in new flexible office space in Prague 5, followed by Prague 1. These districts concentrate demand for premium products, which account for 93 percent of the total flexible workspace stock. Despite this strong expansion, flex offices still represent only approximately 3 percent of Prague’s total office stock.

Prague 4 currently shows the highest number of centres, with 15 locations operated by 10 providers, reflecting strong demand and a well-established office submarket. Prague 5 follows with 14 locations managed by 11 operators. Prague 1 completes the top three most competitive districts, with nine operators across 13 centres. This level of activity confirms the continued attractiveness of the city centre for flexible workspace concepts, despite limited availability of traditional office space and higher headline rents.

Costs and market outlook

The average monthly cost in Prague stands at €187 (CZK 4,530) for a hot desk, €248 (CZK 6,020) for a fixed (dedicated) desk and €338 (CZK 8,200) per desk in a private office. In prime locations, moderate upward pressure on pricing can be expected, driven by the limited availability of modern office space and stable occupier demand. The market is gradually professionalising, with future expansion likely to be selective and demand-led rather than speculative, confirming the segment’s growing importance within Prague’s broader office market.

“The flexible workspace market has gradually matured and today influences not only the design of individual offices, but the entire office sector,” says Pavel Novák. “Both occupiers and landlords are responding to evolving conditions, including higher expectations in terms of flexibility and quality of the working environment, and rising interior fit-out costs. Recently, the pace of expansion has moderated, with operators prioritising portfolio optimisation, stable occupancy levels and operational efficiency over rapid network growth,” concludes Pavel Novák.