Institutional investors are expected to increase their target allocations for real estate investment this year to 9.6 percent up from 9.4 percent in 2014, Colliers International has revealed in its latest research report entitled ‘How long will this property bull market last?’ This seemingly modest increase amounts to an extra US$52.5 billion in the market given the size of the capital pools, which gives a significant boost to overall funds targeting global real estate this year.

It follows a US$105 billion increase on the previous year when target allocations rose from an average of 8.9 percent of existing portfolios in 2013. If these allocation rate increases are applied more widely across private equity and sovereign wealth funds, the total uplifts would amount to US$160 billion in 2014 and US$80 billion in 2015. Total global funds under management currently amount to US$32 trillion.

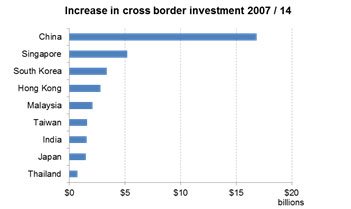

The weight of money targeted at real estate is also evident in the size and origin of cross-border direct investment flows. Although the 2007 peak of US$382 billion is yet to be repeated, cross-border investment amounted to US$262 billion in 2014 with the substantial expansion of Asian investment led by the Chinese. Asian capital accounted for around 13 percent of cross-border investment in 2007 and more than doubled to 30 percent last year, which is a total increase of US$36 billion with signs of further growth.

Walter Boettcher, EMEA Research Director and Economist, Colliers, said: “Weight of capital as an investment driver is certainly not a new phenomenon, but remains undiminished in this particular cycle. However, what is new is the extent to which property investment has become globalised with funds needing to reach beyond their domestic borders to satisfy their target allocations to property. This is driven by the extraordinarily low interest rate environment and an international search for yield, with property offering relatively high returns compared to bonds and equities. The UK and Europe remain primary international targets with funds showing a greater appetite for risk.”

A delayed development cycle has also resulted in an acute shortage of institutional grade product across all markets, resulting in existing ‘standing assets’ being pushed up in value substantially. Debt for development is becoming more accessible, so investors will need to look increasingly at creating their own investible assets through development.

Given the unprecedented weight of capital, Colliers has indicated that there is a once in a generation opportunity to channel investment into the development of productive assets that offer long-term value across the economy. Infrastructure projects such as airports, universities, hospitals and care facilities often have lengthy lead in times and large capital requirements, but offer the long regular paybacks that appeal to institutions.

Walter Boettcher continued: “The real concern for this particular property cycle is that there is too much money chasing the same product. Are there sufficient standing investible assets to satisfy steadily increasing demand? If you think strictly about real estate offering secure long-term income that can be used for annuity liability matching, the answer is probably not, especially given the trend towards short commercial leases.

“Infrastructural development creates the necessary framework for the formation of new geographies that will in turn provide fresh opportunities for the delivery of individual real estate assets. The lasting real estate opportunity is to reshape the property cycle instead of simply moving along a well-trodden path, which requires the industry to take the bold step of considering new opportunities that will facilitate economic growth and with it demand for technically fit, modern commercial real estate.”