CBRE has summarized Q3 2016 results of the Moscow Office market. According to the report, the volume of new construction in CBD in 2017 will return to the levels of 2014-2015 and will reach around 100,000 sqm. Thus, about 75 percent of the new delivery in 2017 will localize in two key submarkets: Moscow-City and CBD.

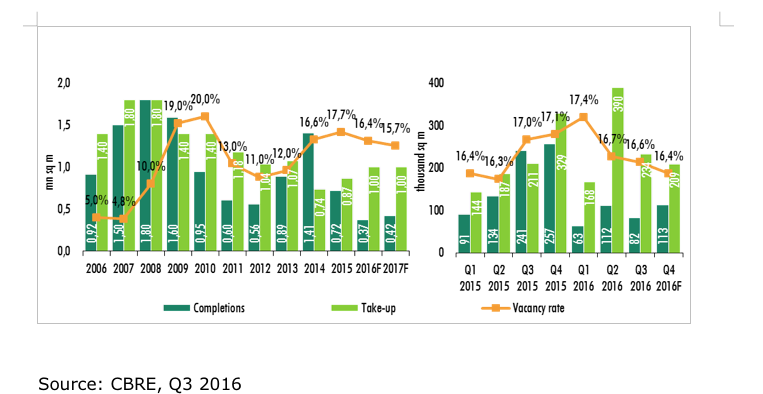

In 2017 completions is likely to amount to 420,000 sqm, over a half of which will be contributed by two office buildings: IQ-quarter (130,300 sqm) and Federation Tower East (82,600 sqm). In Q4 2016 113,000 sqm of new office space is expected to be delivered. As a result 2016 completions volume is not likely to exceed 370,000 sqm, which is twice less than 2015 completions.

Take-up volume in Q3 2016 increased by 10 percent compared to Q3 2015 and amounted to 233,600 sqm. Class B accounted for 65 percent of this value or 152,900 sq m. The volume of transactions for new leases and acquisitions amounted to 790,700 sqm in total since the beginning of year, which is 45 percent above the value in Q1-Q3 2015. Medium-sized office premises with an area of 1,001-3,000 sq m were the most demanded in Q3 2016 (36 percent of take-up).

Tenants and buyers have become more inclined to choose new Class A premises, for which prices and rental rates are still at reduced levels. The volume of new transactions in Q4 2016 may reach 210,000 sqm and 1 million sqm for the whole 2016. After a sharp decline of vacancy rates in Class A in Q2 2016, in Q3 vacancy dropped by 0.1 ppts and stabilized at 19.2 percent.

Change in vacancy rates in Class A resulted in a decline of overall vacancy in the market by 0.1 ppts for the quarter. Vacancy in Class B did not change as a significant amount of new construction (90 percent) contributed to Class B, which effectively replaced absorbed area. The demand values, combined with low levels of new completion will lead decrease in vacancy rate by 0.2 ppts to 16.4 percent in Q4 2016.

Elena Denisova, Senior Director, Head of Office Department of CBRE in Russia said: “Activity in the office market increased in Q3 2016. If in Q2 demand was largely maintained by two large transactions related to the settlement of debt, in Q3 the number of deals transacted at the market terms increased, which suggests that tenants and buyers have begun to make decisions and in some sense aware of the risk of “closing window of opportunity” for getting the best deal in the right building. The volume of lease renewals and renegotiations is gradually declining. We expect that this trend will strengthen in Q4. According to our forecasts, the volume of transactions for new leases and acquisitions of office spaces will reach pre-crisis levels of 2012-2013 by the end of 2016.”