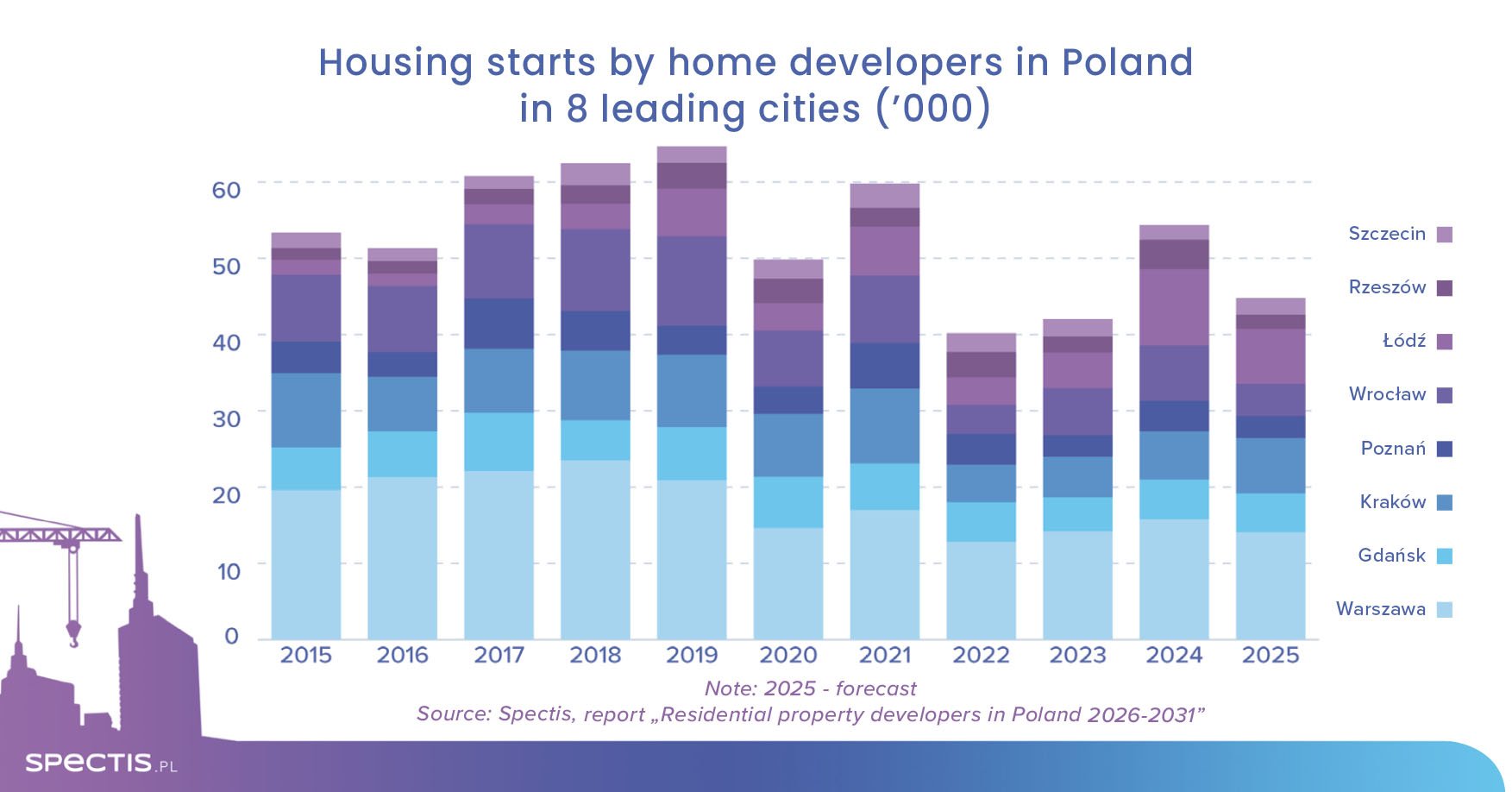

Over the past decade, developers have become the primary driver of Poland’s residential construction sector. Their share of new housing projects has been steadily increasing – from less than half in 2010-2013 to a projected nearly two-thirds in the coming years. An analysis of the financial results of the 60 largest development groups confirms that residential property development continues to be highly profitable, despite occasional market fluctuations. Demand for new housing in major cities remains robust: in 2026-2028, developers are expected to deliver an average of around 135,000 units annually, only slightly below the record years of 2020-2022.

Record revenues of leading developers

According to the research firm Spectis and its report “Residential property developers in Poland 2026-2031,” the total revenues generated by the 60 largest development groups operating in Poland reached nearly PLN 29bn in 2024, of which 88 percent came from residential development sales. This translates into a record-high value of PLN 25bn for the development segment alone. Based on preliminary data, Spectis analysts estimate that in 2025 the sales value of leading developers increased nominally by 4 percent, exceeding PLN 26bn.

Dom Development maintained its position as the market leader in Poland, generating more than PLN 2.9bn in revenues from residential development activities in 2024. It was followed by Develia, Atal, Murapol and Robyg. In 2024, consolidated revenues above PLN 150m were required to be included among the 60 largest development groups, compared to PLN 120m a year earlier.

Stable profitability across the development sector

The rising revenues of the 60 largest developers were accompanied by proportional growth in net profit, which in 2024 exceeded PLN 5bn for the first time in history. In 2021-2024, the group’s net profitability remained remarkably stable, averaging 17.4 percent. Trend analysis for the first three quarters of the year indicates that a similar profitability level is likely to be maintained in 2025, supported in particular by the stabilisation of construction costs.

Ongoing consolidation of the development market

Despite the challenges faced by residential developers in 2025 and the continued uncertainty in the market, two major players opted to pursue expansion through acquisitions.

Develia completed the purchase of 100 percent of the shares in the Polish arm of French developer Bouygues Immobilier (for approx. PLN 280m). Meanwhile, in June 2025, Victoria Dom submitted an application to the Office of Competition and Consumer Protection (UOKiK) seeking approval to acquire assets belonging to the Budner Group.

A growing shortage of attractive land plots, increasing operating costs, market professionalisation and succession issues are among the factors that may drive further consolidation in the Polish development market over the coming years.

Partnerships are gaining popularity in the development market

Alongside acquisitions of local players, various forms of partnerships have become a common strategy for residential developers seeking to enter new markets or strengthen their position. An example is the joint venture agreement signed in October 2025 between Grupo Lar Polska and Galio Group, which plans to deliver several residential projects in Poland, totalling approximately. 1,000 units.

Another notable case is the public-private partnership agreement also signed in October 2025 between Develia and the City of Gdańsk. Under the “Nowy Port 2030+” initiative, the Gdańsk district of Nowy Port is set to be developed and built up, with over 45 buildings planned, comprising more than 1,000 residential units and commercial spaces.

Developers increasingly focus on the PRS segment

Although 2025 was a challenging year for residential developers, many continued to invest in the growth of the PRS (Private Rented Sector) market in Poland. Compared to Western European countries, the Polish PRS market is still at an early stage of development, yet it has shown dynamic growth over the past decade. By the end of 2025, the total stock of PRS housing in Poland reached nearly 30,000 units.

The outlook for the PRS market remains promising. High housing prices in urban areas, limited availability of mortgage loans, increasing social mobility, and changing lifestyles among young people are factors likely to drive further expansion in the coming years. According to announcements from developers active in the PRS sector, tens of thousands of rental units are expected to be delivered over the next five years.