Russia has now overtaken the UK as Europe’s second largest shopping centre market, according to new research from Cushman & Wakefield.

Second only to France, which recorded 17.6 million sqm of shopping centre space at H1 2014, Russia now moves from third position into second ahead of the UK with 17.5 million sqm of space added to the market. The UK follows behind with 16.98 million sqm.

Economic growth and urbanisation has been the main driver of development this year, as developers see potential in densely populated regions with a lack of high-quality schemes, as revealed in Cushman & Wakefield’s latest European Shopping Centre Development report.

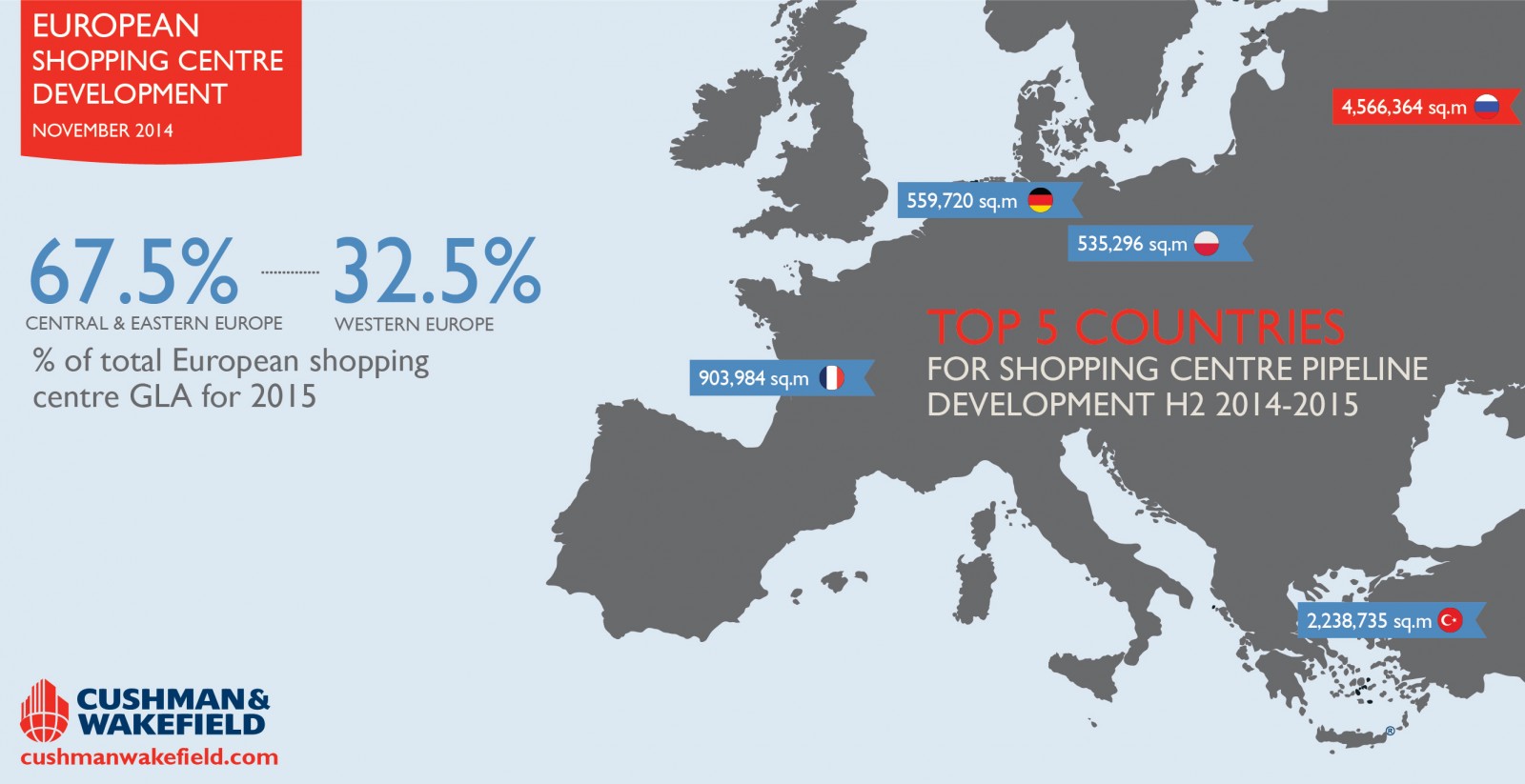

Central and Eastern Europe (CEE), fuelled by frenetic development activity in Russia and Turkey in particular, will account for 81 percent of shopping centre space added to the market by the end of 2014.

Poland is on the third place in CEE and on the fifth place in Europe in terms of the shopping centre development pipeline in H2 2014 – 2015.

Total shopping centre floor space in Europe is estimated to rise to 161.4 million sqm by the end of 2014, a 4.5 percent increase. CEE reached 1.4 million sqm in H1 2014, more than double the 637,000 sqm added to the Western European market.

Russia and Turkey alone accounted for 1.1 million sqm of added space in H1, as developers aim to catch-up with the Western European market, focusing on larger centres that serve a wide catchment area. More than 100 new shopping centres will have been developed in Russia over a two year-period by the end of 2014.

A further 4.57 million sqm of space in the development pipeline is expected to be delivered to the Russian market between H2 2014 and 2015 – this could see the country overtake France as Europe’s largest market. One of these developments in Russia is Europe’s largest mall, Moscow’s Avia Park, which spans 230,000 sqm and is anticipated to complete before the end of the year.

In H1 2014, there were 53 new malls in Europe with 12 of them in Russia – a further 49 are scheduled to be finished by the end of 2015.

Cushman & Wakefield’s head of retail services in Russia, Maxim Karbasnikoff, said: “Russia is now the largest consumer market in Europe but until very recently supply was not meeting demand. Strong development activity witnessed in Russia since 2010 has led to a very large pipeline now being delivered. However, political uncertainty, steady depreciation of the rouble and stagnating consumer demand is pressurising retailers. Nevertheless, fundamentals are still positive in the mid-term and we expect vacancy to stablise and rents to reach a healthier level in the coming six months.”

Magdalena Sadal, Senior Research Consultant at Valuation & Advisory of Cushman & Wakefield, said: “In Q3 2014 in Poland there were 432 shopping centres (including traditional and specialized shopping centres, retail parks and outlet centres) totalling 10,158,275 sqm GLA. Shopping centres account for 90 percent of the total stock (385 traditional and specialized ones), with retail parks making up 8.3 percent (37 schemes totalling 845,110 sqm) and outlet centres 1.6 percent of the total (currently 10 facilities with another 2 under construction). New retail space supply in the first 3 quarters of 2014 was 317,500 sqm, up by 42 percent on the figure recorded in the same period of 2013, in 14 new retail schemes and three extensions. Extensions accounted for around 5 percent of the new floor space provision in 2014. The biggest retail scheme completed so far in 2014 was Atrium Felicity in Lublin (75,000 sqm), which opened in March, being also the largest shopping centre scheduled for 2014. The second biggest is Galeria Warmińska in Olsztyn with 41,000 sqm GLA, opened in September. Around 850,000 sqm of new retail space is under construction, of which around 150,000 sqm is expected to come on stream by the end of December 2014.”

She added: “According to the latest estimates, Poland’s modern retail supply will total 470,000 sqm in 2014, a fall of 24 percent on 2013’s record figure. Apart from significantly smaller volume, the other determinant of the 2014 modern retail space supply is that smaller-sized schemes are developed in minor markets. Only 47 percent up-to-date supply of 2014 was opened in towns larger than 100,000 population, however, with no opening in a large city, whereas in 2013 67 percent of the new retail space was opened within the 8 agglomerations. Demand for retail space remained at a healthy level in the first three quarters of 2014. Tenants focused on established retail schemes offering high footfall and satisfactory revenues. Re-marketed shopping centres are an attractive alternative to newly-constructed space. Due to the current demand level, the marketing period for new schemes has become much longer and few shopping centres are fully let when they open. Vacancies in newly-opened retail schemes are at average 10-15 percent whereas average vacancy on mature markets is ca 3 percent.”