The residential market in Bucharest opened 2026 with an 18.6 percent year-on-year decline in apartment transactions during January–February, according to an analysis by Crosspoint Real Estate, the International Associate of Savills in Romania. In neighbouring Ilfov, transactions also fell, albeit at a more moderate pace of 10.9 percent.

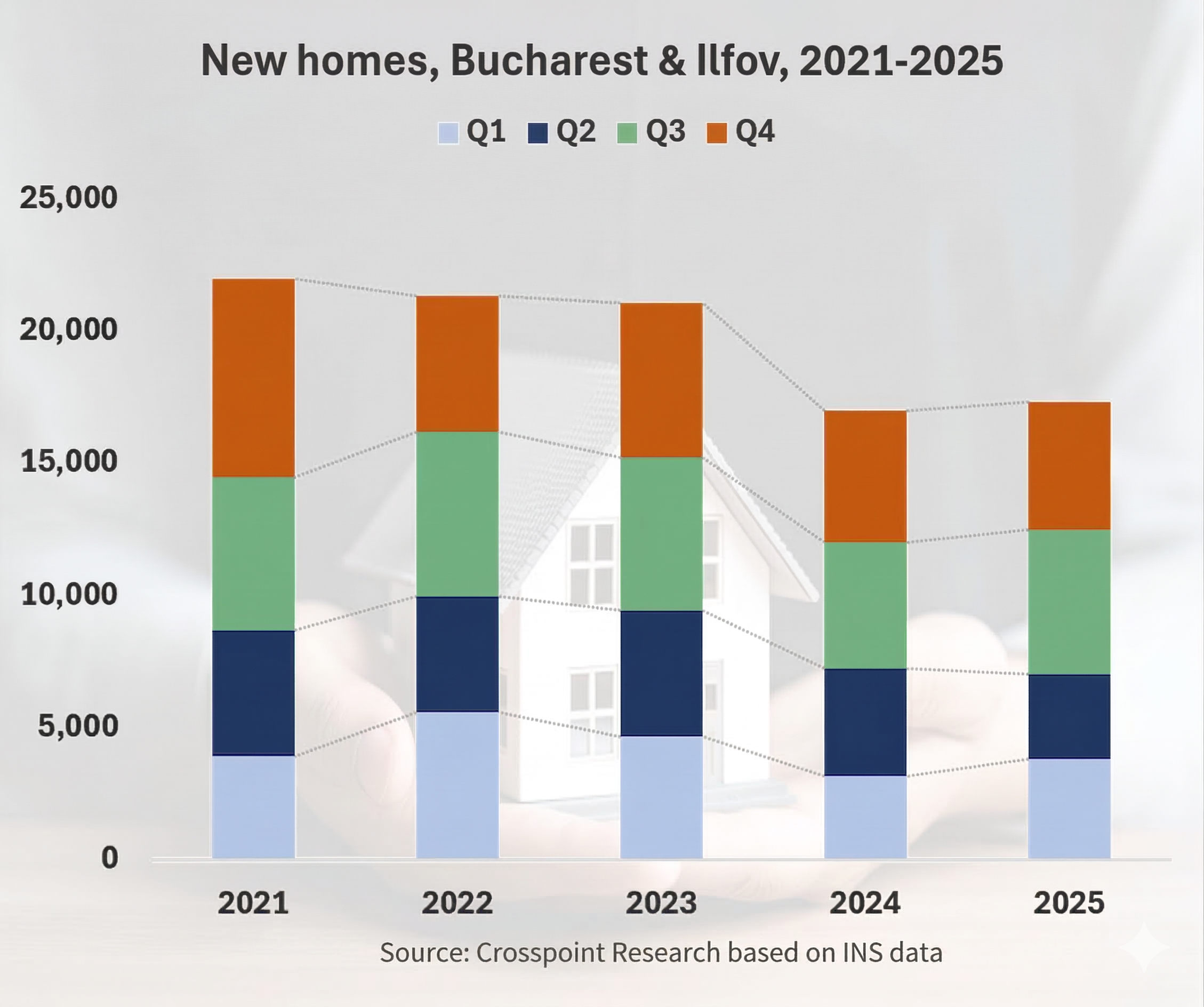

These figures follow a 2025 in which the total transaction volume in the Bucharest–Ilfov metropolitan area had already dropped 8.5 percent compared to 2024, to 55,297 units, while prices for new units rose by approximately 20 percent, reaching an average of €2,500/sqm.

“What we are seeing in the market now is the consequence of an accumulated permitting deficit over several years, overlapping with pent-up demand and a shifting regulatory framework”, explains Oana Popescu, Head of Residential at Crosspoint Real Estate, International Associate of Savills in Romania. “The residential projects we take on from the concept phase reflect an increasingly selective approach by developers. We are talking about fewer units, better positioned, with a product calibrated to the segments that better absorb cost pressure. This evolution has also been reflected in our portfolio mix, which has clearly shifted toward middle-high and premium segments that together now account for 80 percent of our residential consultancy activity.”

The residential market entered 2026 with the most constrained pipeline in the past five years, with only 4,013 building permits issued in 2025 in the Bucharest–Ilfov area. The 5 percent increase in this indicator in 2025 compared to 2024 remains marginal relative to the deficit accumulated in recent years.

At the same time, the 2 percent growth in deliveries recorded last year compared to 2024, reaching 17,293 newly completed homes in Bucharest–Ilfov in 2025, came in a context where the reduced 9 percent VAT rate was conditioned, from August 2025 onward, on apartment delivery by year-end. Developers therefore accelerated construction to meet this deadline, and the delivery figure partly reflects an artificial increase driven by the fiscal calendar, rather than a production capacity that will be sustained into 2026.

Additional pressure comes from the entry into force of Law 207/2025, which intervenes in a market that delivered less in 2025 than in any year during the 2019–2022 period. While the regulation addresses a genuine gap in buyer protections and represents a step toward European standards, the side effect on the pipeline will be visible. Projects that relied on off-plan sales to finance construction phases will face additional difficulties, and some planned developments will not reach the execution stage.

“2026 is a year of recalibration, not crisis. Buyers who understand that new supply will remain limited over the next two years and that prices within Bucharest will not see structural declines have a decision window before the supply pressure becomes even more visible. The market has matured, and the purchasing decision has become more rational, focused on total cost and long-term quality. This is a healthy development for all participants involved,” said Valentin Neagu, Managing Director of Crosspoint Real Estate.

The likely outcome is an even more constrained supply in the 2027-2028 horizon, which will sustain price pressure, particularly in central areas and in the premium segment, where northern Bucharest, with average prices already exceeding €3,500/sqm, remains the most active part of the market.

Construction costs: Romania among the highest increases in Europe

Beyond transaction dynamics, the most significant pressure on the market comes from production costs. Eurostat data included in the Romanian Real Estate Market Report 2025, published by Crosspoint Real Estate in March, shows that Romania recorded one of the sharpest increases in construction costs for new residential buildings in Europe, 9 percent in 2025, compared to approximately 1 percent at the EU average. The gap relative to the European average has widened steadily since 2022, and its effects are now visible both in final apartment prices and in the caution with which developers approach new projects.

The macroeconomic backdrop against which this correction is unfolding remains challenging: average annual inflation of 7.3 percent in 2025, the highest in the EU, a net average wage of €1,120 in December 2025 and a deteriorating labour market, with the unemployment rate rising to 6 percent. Affordability remains a structural challenge, and purchasing an apartment in Bucharest currently requires the equivalent of seven to nine years of average net income.

A visible market recovery is anticipated for 2027, when inflationary pressures are expected to ease, and the full effects of the new regulatory framework will be better integrated into developers’ strategies.