As indicated by the results of PMR’s latest report, entitled “Construction sector in Kazakhstan 2016. Development forecasts for 2016-2021”, construction industry output increased by 4.4 percent in real terms to KZT 2,861 billion (€11.6 billion) in 2015. In recent years, the construction industry in Kazakhstan has been fuelled overwhelmingly by new construction projects, whereas initiatives involving extensive modernisation and repair have diminished in value.

Last year, the only driver behind the estimated 4.4 percent year-on-year increase in construction output was the area of new construction, which expanded by 8.5 percent. The subdivision of extensive renovation was decreased by 24 percent, whereas that of minor repairs was reduced by 9.4 percent. Given that minor repairs and extensive renovation were responsible together for only 11.5 percent of the country’s construction output last year, the significant negative performance of these subgroups in 2015 diminished the construction industry only moderately.

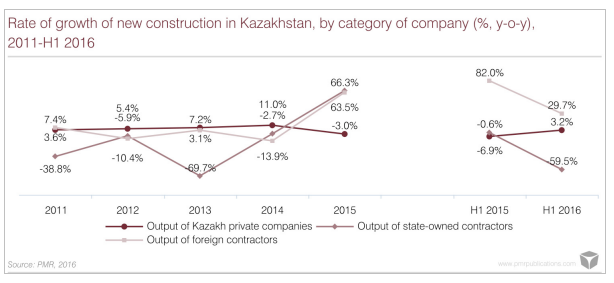

In 2015, Kazakh private companies accounted for 76.1 percent of all construction output in the country, and were followed by foreign entities, which accounted for 23.2 percent. State-owned enterprises accounted for an insignificant 0.7 percent of total output.

The share of new construction as a proportion of total output rose from 82.3 percent in 2012 to 88.5 percent last year. Until 2015, new construction projects had increasingly been rolled out by private Kazakh companies, whereas there had been a reduction in the exposure of foreign and state-owned companies. Since 2015 the market share of foreign contractors has increased notably, as the total value of new construction output generated by foreign contractors in 2015 rose by 63.5 percent in year-on-year comparison and by almost 30 percent in H1 2016.

According to PMR, in recent years the most dynamic construction activity has been observed in the residential sector. The total floor area of residential properties listed in official records in Kazakhstan in 2015 came to 8.94 million sqm, which is almost 19 percent more than that of 2014, standing for the record annual housing completion result recorded in Kazakhstan in more than two decades. The uptrend in housing space registration is very likely to continue in 2016, as 17 percent more space was activated across the country in the first half of the year than in H1 2015.

Home sales and construction activity in Kazakhstan continue to display impressive growth, regardless of the weak overall economic activity in the country. The Kazakh economy increased by only 0.1 percent in the first half of 2016 and GDP is expected to rise by only around 0.3 percent for the full year. Nevertheless, in H1 2016, 13.1 percent more home sales were registered in Kazakhstan than in the corresponding period a year earlier. Furthermore, there was a 6.6 percent real increase in construction output in the first half of 2016, though growing largely on projects rolled out in Astana. The double-figure growth in construction activity in Astana is being boosted by the preparations for the World’s Fair EXPO-2017, which is to be held in the city next year. It is worth mentioning that both performances were not reached on low base effect, as solid positive figures were also achieved in the same period last year.

Ageing and obsolete industrial capacities are among the key hindrances to more vibrant economic progress in Kazakhstan. The construction, replacement and modernisation of operational industrial units across the country will continue to propel growth in the coming years, thus boosting investment in industrial construction, and in manufacturing in particular. The sharp devaluation of the tenge which occurred between 2014 and 2015 has made exports more competitive. This year the positive dynamics in construction will be also supported by the Nurly Zhol infrastructure development programme. The Programme’s funds ($14-20 billion) are scheduled to be spent between 2015 and 2017 (or even until 2019) and will be used for the construction of transport and social infrastructure, utility network modernisation and the provision of additional subsidised loans for SMEs. In particular, the programme should have a positive direct impact on civil engineering.

However, the national currency’s devaluation that accelerated in August 2015 has substantially hit the domestic mortgage market and particularly those holding foreign-currency loans. In January-July 2016, the national currency fell year on year by 46 percent against the US dollar. Mostly because of this fact, the proportion accounted for by overdue payments had increased to 8.8 percent by the end of 2015 and further to 9.0 percent by the end of June 2016. Between mid-2014 and mid-2015 the proportion accounted for by overdue payments was constantly falling. At the end of June 2015 it accounted for only 7.3 percent of the total value of outstanding loans granted to population for construction and purchase of a residence, a 3.3 p.p. reduction over the previous twelve months. The last occasion on which a lower proportion was seen was in 2011.