2017 was the best ever for Poland’s industrial market – gross demand totaled 3.9 million sqm, summarized advisory firm JLL on the industrial market in Poland in 2017.

“Total space leased under new agreements and expansions in 2017 exceeded 3.1 million sqm, which is nearly 1 million sqm more than in 2016. Once lease renewals are added, the gross take-up rises to more than 3.9 million sqm. Retailers and logistics operators continued to drive the market, together accounting for more than 65 percent of net take-up in 2017, including some excellent e-commerce transactions featuring the likes of Amazon and Zalando. A strong third position was retained by the light manufacturing sector contributing 20 percent of net take-up,” commented Tomasz Olszewski, Head of Industrial CEE, JLL.

The combination of ideal location, developed modern infrastructure and attractive rents was the main reason for Central Poland being the hot spot on the Polish map in 2017, with nearly 30 percent of total net take-up attributable to that region alone, driven mainly by retailers. Due to tightening labor market conditions, attention has also turned to emerging markets, which together saw deals for approximately 400,000 sqm (13 percent of total new demand). In 2017, the Lubuskie region came to the fore in terms of demand, with more than 150,000 sqm of tenant-secured space.

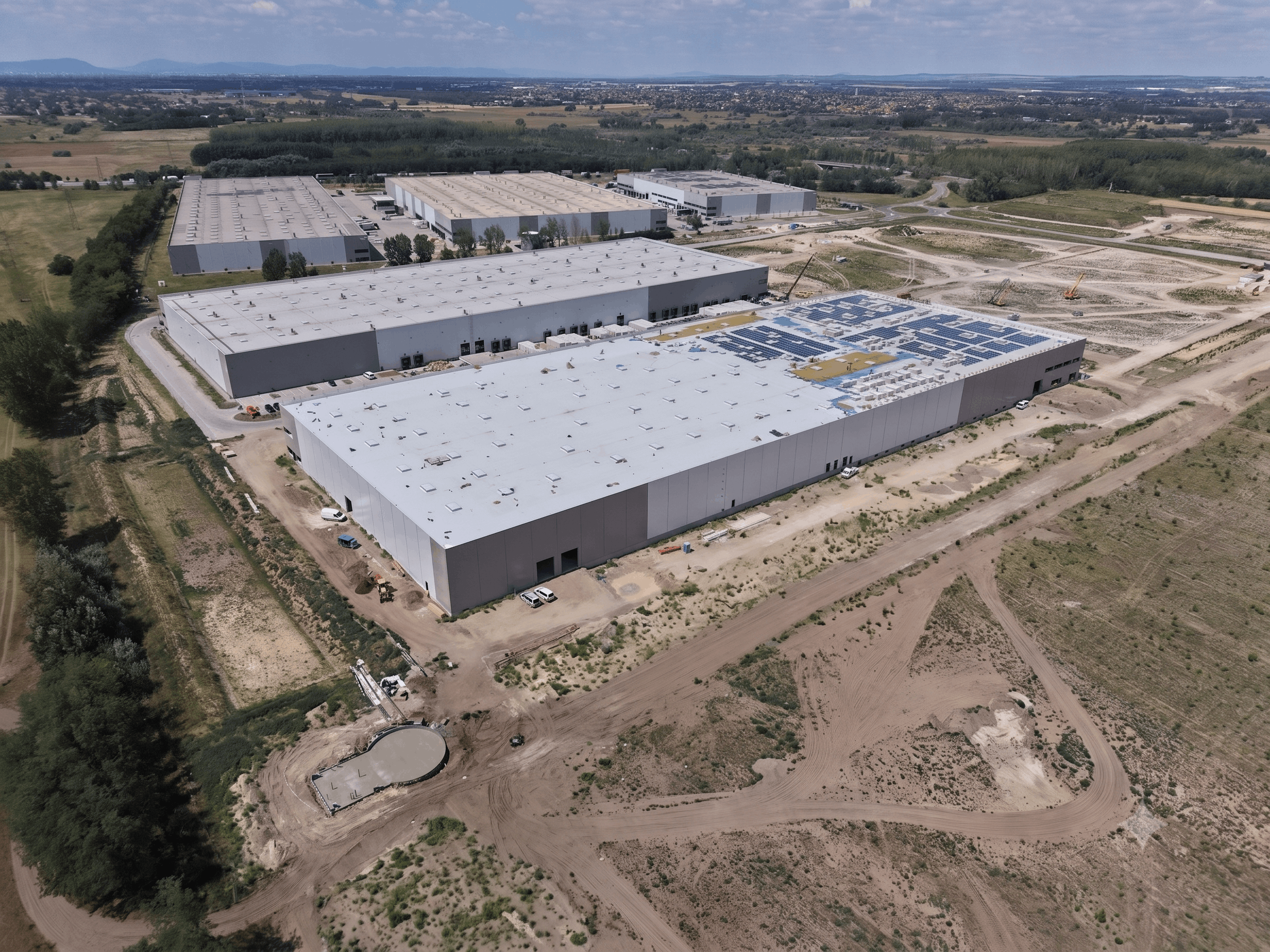

“This outstanding leasing market performance was accompanied by an all-time-high volume of new completions. The warehouse market in Poland grew by another 2.3 million sqm, over one million sqm more than in 2016. Over the past five years, market has almost doubled, bringing stock levels up to 13.5 million sqm by the end of 2017, just behind Italy’s 15.1 million sqm. This gives Poland a solid eighth place in the European Union in terms of total stock,” added Jan Jakub Zombirt, Associate Director, Strategic Consulting, JLL.

The five markets with the highest growth results were Warsaw Suburbs, Upper Silesia, Szczecin, Central Poland and Poznań, which together accounted for almost 75 percent of newly developed space. The largest projects were built for representatives from the e-commerce sector.

“There is 1.2 million sqm in the under-construction pipeline. The most active regions are still Upper Silesia with 360,000 sqm, Central Poland with 300,000 sqm and Warsaw with 210,000 sqm. A market worth noting is Lubuskie: more than 130,000 sqm of modern industrial space is being constructed there,” commented Jan Jakub Zombirt.

New locations, higher warehouse standards and adjustments to specific tenant needs have led to the increasing popularity of BTS (build-to-suit) projects. As a result, speculative construction is at a low level: more than 72 percent of the pipeline is already secured by lease agreements. Interestingly, the major markets are no longer the only locations for speculative projects, as still unsecured space is also being constructed in the Kujawy, Kraków, Szczecin and Lubuskie regions.

Despite such an impressive pace of market growth the vacancy rate in Poland remained stable, standing at 6 percent at the end of 2017.

The industrial market in Poland did not see any major changes in the level of rents during Q4 2017. The highest prices for warehouse space were in Warsaw Inner City and Kraków, where headline rents ranged from €4.1 to €5.1 / sqm / month and €3.8 to €4.5 / sqm / month, respectively. The most attractive rents for big box units were consistently found in Central Poland (€2.6 to €3.2 / sqm / month), Upper Silesia (€2.8 to €3.6 / sqm / month) and Poznań (€2.8 to €3.5 / sqm / month). Some markets have recently seen slight increases in the lower rental band and further upward pressure on rents is anticipated in the next few quarters. The rents above do not include incentives from landlords and should be treated as a basis for negotiations.