Logistics real estate managed to stand its ground in 2023, emerging as one of the most attractive segments despite its modest investment volume. The initial signs of a positive dynamic seen during the second half-year have kindled hopes that the investment market will revive and open up interesting opportunities. The increase in key lending rates has proven an effective countermeasure, bringing inflation down faster than expected. Many market analysts now predict a decline in interest rates and therefore a drop in financing costs by mid-year 2024, with corresponding downstream effects on yield rates, which had experienced significant decompression over the past years.

“The pricing phase on the investment market for logistics real estate is gradually drawing to a close. In 2024, attractive market opportunities will emerge and mark the onset of the next investment cycle,” said Tobias Kassner, Head of Research and Member of the Executive Board at GARBE.

By contrast, the rental market is slow to transition to the new market cycle and is retarding the rent performance, which has been dynamic so far, in a variety of ways, depending on the regional availability of space and the local economic development.

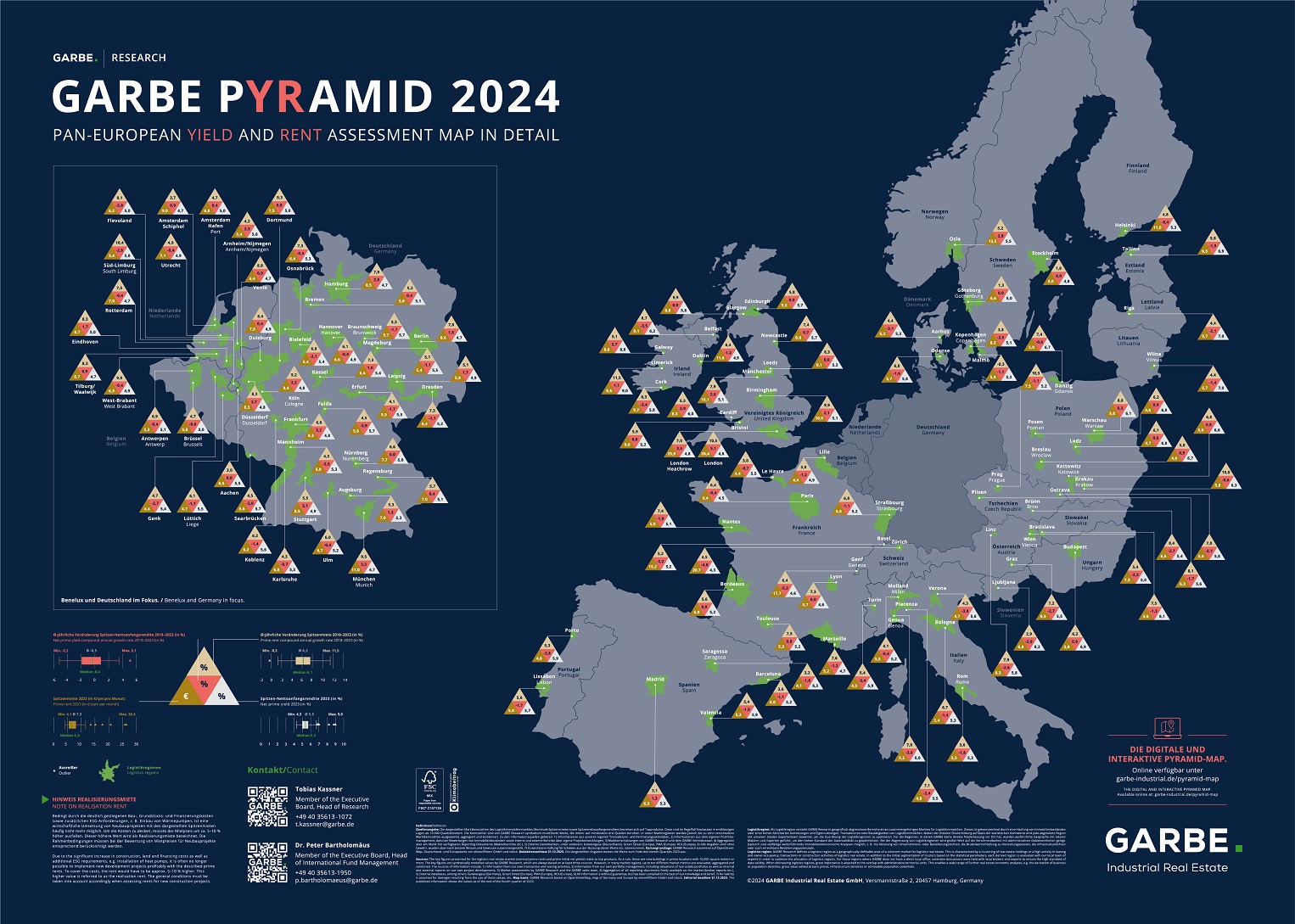

These are the findings that GARBE Research presented in its GARBE PYRAMID MAP for early 2024, the latest update of the company’s overview of prime rents and prime net initial yields for the 112 leading logistics real estate submarkets in 23 European countries.

European Investment Market

In response to the drastically changed geopolitical and finance policy parameters of the past two years, operators on the European investment market for logistics real estate showed noticeably more restraint in 2023 than they had in previous years. During the first nine months of the year, the transaction volume took a nosedive, declining by around 58 percent over the prior-year period. Other asset classes presented a similar picture. Investments in office real estate, for instance, dropped by more than 60 percent across Europe.

But after bottoming out during the first quarter, the transaction volume recovered successively. Softening real estate prices and the prospect of an end to key lending rate hikes have encouraged a first group of investors—notably equity-rich players—to exploit the opportunities that market corrections presented in recent months. However, the transaction volume was well below the level of previous years.

Dr Peter Bartholomäus, Head of Fund Management & Capital Markets, Member of the Executive Board at GARBE, elaborated: “In the eyes of investors, logistics real estate stood its ground as an asset class in 2023. With its low vacancy rates, demand still strong in many regions when compared to available supply, and the prospect of further potential for rent growth, it outperformed office and retail real estate, for instance. In fact, in some European markets, such as Germany or Italy, logistics investments have lately claimed the largest share of the overall investment market.”

A look at the past eighteen months reveals a slowing decompression dynamic. With a gain of 50 basis points, the fastest increase in yield rates was registered during the second half of 2022. In 2023, prime yields went up by roughly another 55 basis points, with the rate of increase higher during the year’s first half (+35 bps) than during its second half (+20 bps).

In top markets like the United Kingdom and the Netherlands, the average rise in prime yields was down to seven and ten basis points, respectively, during H2 2023. Indeed, prime yields in some eastern European markets, including the Baltics and Slovakia, but also Switzerland, saw no change at all. Such trends usually herald the onset of the next cycle, and this is particularly true for the British market. Seen in the context of a prospective reduction in key lending rates by the summer of 2024, this suggests that we are gradually nearing the decompression peak.

At the end of 2023, the priciest markets were located in Germany, the Netherlands, France and Switzerland. Topping the list was the Zurich logistics region with a prime net initial yield rate of 4.3 percent. Next came Paris (4.5 percent), Geneva and Lyon (both 4.6 percent). In German and Dutch top markets such as Berlin, Hamburg, Munich, Amsterdam and Rotterdam, prime yields are currently at 4.7 percent. In some markets, prime yields for logistics real estate undercut those for office real estate.

European Occupier Market

The occupier market, too, is showing signs of a gradual stabilisation. As a result of the sluggish economy in the European Union and due to slow global demand, companies remained on the fence during the first half of the year. But during the third quarter, take-up experienced a significant surge, exceeding the Q2 total by 20 percent. It admittedly failed to match the record levels of the two preceding years. Still, demand has normalised and is now on a level with pre-pandemic times.

The cross-European vacancy rate went up to 5.2 percent in the year as a result of flagging demand. But since building activities—especially the construction of speculative schemes—are clearly in decline, vacancies cannot be expected to keep increasing at the same brisk pace.

The normalisation of the demand for space has also impacted rental growth. While prime rents still increased by 6.8 percent during the second half of 2022 and by 6.5 percent during the first half of 2023, the growth slowed to a mere 3.1 percent or 0.22 euros/sqm during the second half of 2023.

A drilldown by country and region reveals stark differences in dynamic though. Above-average increases were registered in the Netherlands (+6.6 percent) and Austria (+4.7 percent). This contrasts with the situation in other markets like the Czech Republic or Denmark, which reported a stable trend.

Outside Germany, the logistics regions seeing the fastest rent growth during the second half-year were mainly located in the Netherlands: Tilburg/Waalwijk (+15.5 percent), West Brabant (+12.5 percent), Rotterdam (+11.3 percent) and Amsterdam/Schiphol (+8.4 percent). Another region with significant rent growth (8.5 percent) was the Paris metro area. On the whole, the average prime rent in Europe increased by almost 2.00 euros/sqm up to 7,35 euros/sqm (+36 percent) over the past five years.

Outlook

Tobias Kassner, summarised: “The investment market has picked up a little steam, having lingered on a low level during the second half of 2023. Its robust metrics make logistics real estate a more attractive and safer asset class for many investors than office real estate. This is true for core assets as much as for value-add properties. Given the prospect of interest rate cuts by the summer of 2024, as announced by ECB President Christine Lagarde, there is a good chance that financing costs may come down during the second half of the year.”

Until then, it is safe to assume that prime yields will continue to decompress slightly or remain largely unchanged, depending on how the market cycle progresses. The gradual recovery of the investment market, which already started in the second half of 2023, will continue in 2024. Equity-rich developers and asset managers who have performed well in recent years stand to benefit from this market phase because the devaluation of the market and possible fire sales could create nice opportunities.

Kassner went on to elaborate: “Elsewhere, we are inclined to expect stabilisation. If the inflation continues to subside, it will have a positive effect on consumption patterns and the export of goods in Europe.”