JLL has released a summary on Q1 2015 of Poland’s industrial market as well as an outlook on the sector’s key trends for the coming months.

Tomasz Olszewski, Head of Industrial CEE, JLL, said: “The industrial market maintained its momentum in Q1, with gross demand for warehouse, logistics and production space reaching nearly 585,000 sqm. This result was the busiest ever beginning to a year. Moreover, total modern warehouse stock hit the 9 million sqm threshold. Construction activity remains buoyant and nearly 593,000 sqm of space is currently at the development stage across Poland.”

Gross demand for warehouse, logistics and production properties hit nearly 585,000 sqm in Q1. Occupier activity in Q1 was highest in Central Poland, where tenants leased or renewed a total of 141,000 sqm. Poznań and Upper Silesia were next with gross leased volumes of 92,000 sqm and 86,000 sqm respectively.

Jan Jakub Zombirt, Senior Research Analyst, JLL, commented: “Net demand – excluding lease renewals – in the first quarter stood at 380,000 sqm. Interestingly, a number of large lease transactions in Q1 were concluded in regions which are not considered typical industrial locations, including, i.a., Szczecin, Toruń or Podkarpacie. New leases totalling 107,000 sqm were signed outside of the five major markets, translating into a 28 percent share of total net take-up. This can be viewed as a very good result as the share of these less well-known regions of Poland’s total stock is only 8 percent.”

Interestingly, 50,000 sqm of the 70,000 sqm of new leases in Central Poland, were signed in Piotrków Trybunalski, the highest volume in years resulting in a substantial fall of available space in the area.

The largest lease transaction signed in Q1 involved Jysk, which leased 40,000 sqm in Piotrków’s Logistic City.

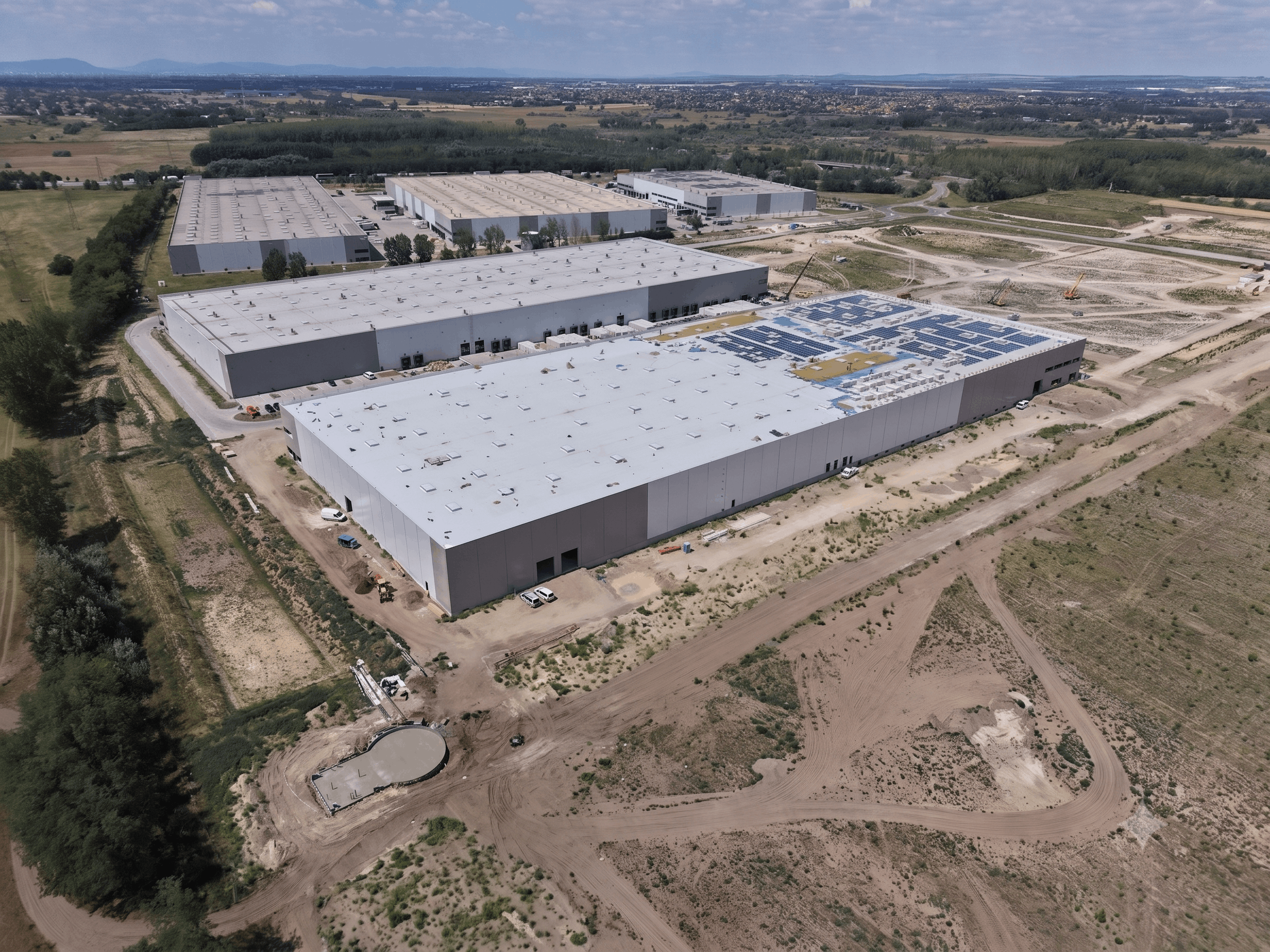

At the end of Q1 2015, total modern stock in Poland stood at 9,02 million sqm. In terms of market share, more than a half of the existing stock is today in the hands of the four largest market players and their JV partners (Prologis, SEGRO, Logicor and Goodman).

New supply completed during the quarter was 298,000 sqm. The lion’s share of the new space was found in the Poznań market (189,000 sqm), followed by the Warsaw Suburbs (28,000 sqm) and Tri-City (27,000 sqm).

Construction activity remains buoyant, with nearly 593,000 sqm currently at the development stage. The regions with the largest amounts of space now under construction are Wrocław (101,000 sqm), Upper Silesia (92,000 sqm) and Poznań (63,000 sqm). Today, construction activity is found in almost every region.

“We have observed a further increase in the share of speculative projects. At the end of Q1, projects which were underway but did not have a secured tenant totalled 215,000 sqm, which translates into 36 percent of the space currently under construction,” Tomasz Olszewski added.

According to warehousefinder.pl, at the end of Q1, the vacancy rate stood at 7.3 percent, which was down from 9.8 percent in Q4 2014. Of the five major regions, the largest share of immediately available space was found in both Warsaw zones (13.9 percent in the Inner City and 10.3 percent in Warsaw Suburbs). The sharpest decrease in vacancy rate was seen in Central Poland, where, on the back of a few large deals in the Piotrków Trybunalski area, the region’s rate dropped from 15.8 percent in the previous quarter to 6.1 percent.

A slight fall in headline rents was seen in both the Upper Silesia and Poznań markets, where they now range from €2.9 to €3.6 sqm/month and €2.8 to €3.5 sqm/month respectively. Rents in the remaining regions remained stable throughout Q1.