Affordable rents for office space in the centre of Prague have surpassed €30 per sqm per month for the first time, reaching a historic high. At the same time, Prague maintains a long-term low vacancy rate of just 7.0 percent, the lowest of any CEE capital. Only one building was completed in the first quarter of this year, and new construction is expected to fall this year to its lowest level in more than a decade. This is according to an analysis of the office real estate market by Colliers.

The lowest volume of new supply in more than a decade

The first quarter of 2025 brought only one completed building to the Prague office market, the first phase of the E-Factory (Pragovka) project with 8,700 sqm of industrial-style modern offices. Four more projects with a total area of 17,900 sqm are expected to be completed by the end of the year, making the resulting volume of new construction for the whole year the lowest in the last ten years. “The outlook is significantly more positive, with up to nine projects with a total area of 160,900 sqm scheduled to start construction between Q2 and Q4 2025, with completion between 2026-2028,” says Josef Stanko, Director of Market Research at Colliers.

The market also continues to see a trend of refurbishments: two were launched in the first quarter. The 1980s-era building in Prague’s Pankrác district, now called Isola, will undergo modernisation and offer 8,200 sqm of sustainable office space in 2026. Another interesting project is the reconstruction of the Kotva department store, which will bring exclusive offices, whose completion is scheduled for the end of 2027. “More and more often, we are also seeing the conversion of old office buildings into residential projects. Given the acute shortage of housing in Prague, this approach is economically logical, but it does not help the office market much. On the other hand, it can contribute to the creation of a balanced mix of functions, which will prevent the creation of office ghost towns,” comments Josef Stanko.

Lack of vacant space puts pressure on the market

The Prague office market has a total of 3.96 million sqm of modern office space with a vacancy rate of just 7.0 percent. Prague thus holds the lowest vacancy rate of all CEE capitals, forcing some tenants to postpone or cancel their plans for new offices altogether.

All of Prague’s key office hubs show occupancy rates between 93.7 percent and 96.1 percent. The Budějovická area is an exception with an occupancy rate of over 99 percent, but a local tenant Česká spořitelna, has started to divest its current property portfolio, creating uncertainty about the future of the entire location.

Of the 278,000 sqm of vacant space, buildings completed in the last three years account for a quarter of the space, and another quarter consists of projects from 2009 to 2021. Only 19,000 percent are available, representing just 0.5 percent of the so-called grey vacancy.

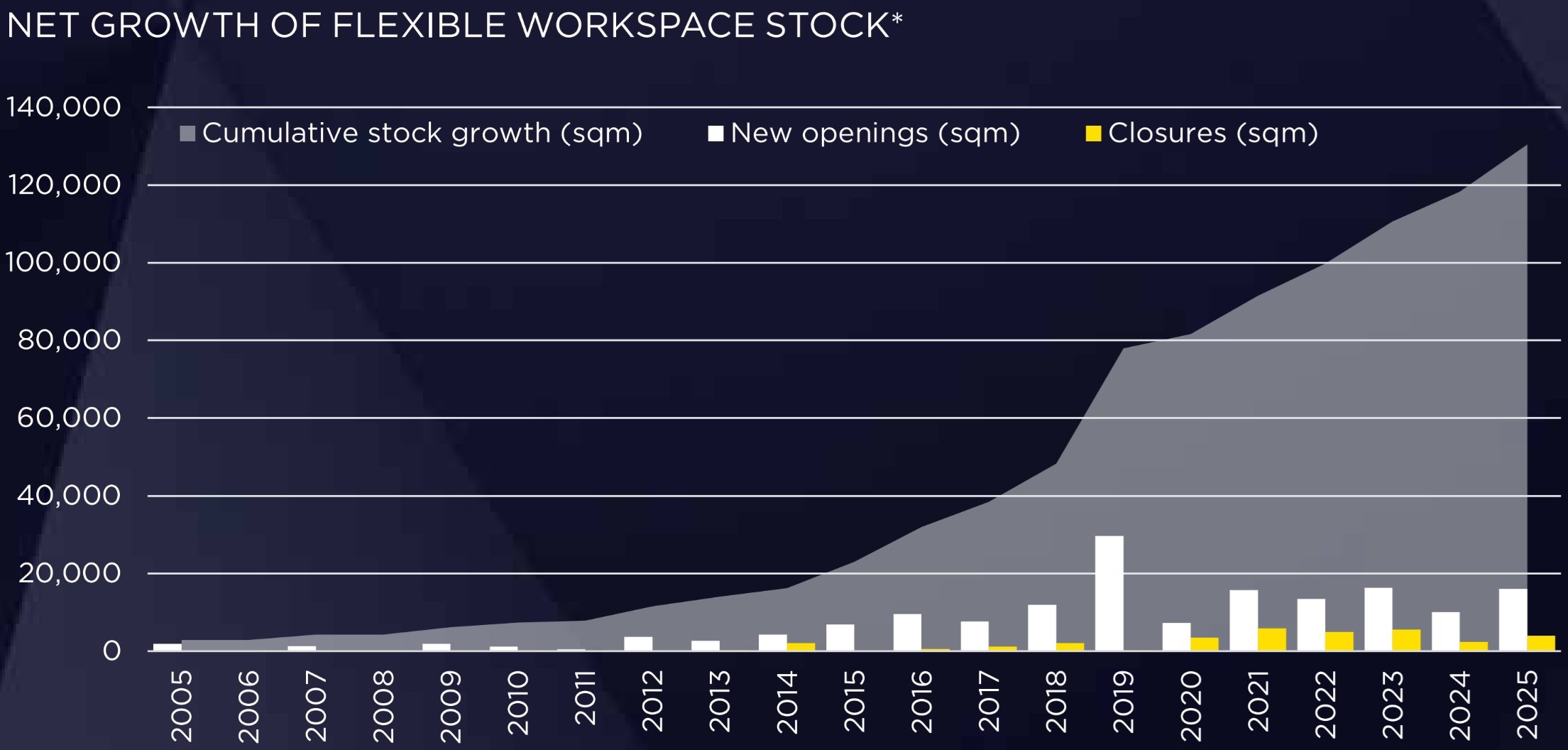

Flexible offices off the radar

The flexible office segment has seen minimal activity. Scott.Weber continues to prepare centres in Smíchov and the historic NR7 building, while IWG will open a centre in the Lighthouse project in Holešovice and a new Signature centre in Pankrác Prime. On the other hand, the Regus centre in Prague City Centre has been closed. “Flexible offices account for less than 3 percent of the market in Prague, and only some of the centres are suitable for corporate clients. This is often by design, given that the event design or startup communities require a different approach to running a centre,” explains Josef Stanko.

Demand is at its lowest level since 2020

Although there is considerable activity in the market, the first quarter saw relatively low gross realised demand. It was 87,700 sqm, the lowest volume since 2020. Net take-up was 47,900 sqm with a share of 55 percent, with renegotiations accounting for 40 percent and subleases the rest. Pre-lettings fell to a negligible 1 percent of the volume of take-up. In particular, due to the absence of speculative construction in recent years, only about 38,500 sqm is available in completed offices across the city. The fact that ČEZ confirmed the purchase of the remaining three buildings in the Smíchov City project also had an impact. “We know from experience that pre-construction transactions do not take place en masse, so now our options are mainly focused on projects with an imminent start for construction,” adds Josef Stanko.

Historic milestone: rents of EUR 30 per sqm in the centre

In the first quarter of 2025, the reference rent rate in the centre of Prague reached €30 per sqm per month for the first time. This level has been extended from individual premium projects to the wider city centre area. “We are aware that some projects have been asking for and achieving such rents (and even higher rents) for some time, but we are only now seeing that the market is mature enough to extend this level of rent to a wider area. The same applies to the main office locations around the city centre,” comments Josef Stanko.

Rents in the wider city centre locations have risen to €20/sqm/month, while in the outskirts they remain at €16.50/sqm/month. For typical class A buildings near metro stations, average rents have increased by 3.3 percent year-on-year and by 6.3 percent over two years to the current €17.4/sqm/month. Rising rents are leading tenants and landlords to form long-term partnerships, often to enter into leases of 7 or 10 years. With standard re-letting of existing office space, long-term leases are also preferred due to costly fit-out, the space’s book value and its future depreciation.