Retail property is in strong demand across most of Europe and investors are not only turning to new markets but also taking on more risk as they seek out opportunities. Volumes rose 25 percent in the last year to their highest since Q2 2008, taking market share from other sectors and putting more pressure on prices. Shopping centre yields are down 26 basis points in the past 12 months, now averaging 6.1 percent across Europe.

The market is more concerned about finding quality stock than exactly what sector it is in however and retail saw its market share fall back in Q3 as other sectors provided more opportunities. Retail volumes fell 24 percent between Q2 and Q3 while industrial rose 17 percent and offices 8 percent. In part this is a reflection of the distortion caused by some of the large trades conducted in Q2 and also a lack of new high quality retail opportunities coming forward in some markets.

According to Michael Rodda, Head of EMEA Retail Capital Markets at Cushman & Wakefield, this is likely to prove a temporary dip. “Since the summer we’ve seen a lot more stock being prepared for marketing and while much has been secondary, investors are interested where they can see value and recovery potential. What is more we’re also seeing a lot of high quality schemes and high street assets now coming forward. As a result we’re anticipating a very strong quarter and perhaps the best Christmas the retail property sector has had since 2007,” he said.

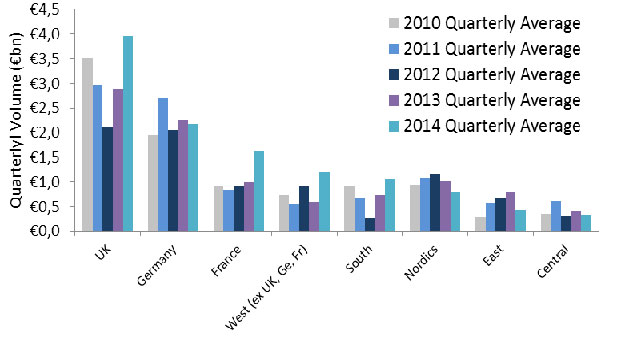

Low risk mature markets remain in high demand, with the UK followed by Germany and Sweden favoured for short-term retail turnover growth but others such as France facing strong demand despite a more lacklustre sales outlook. The core countries of Germany, the UK and France drew a market share of 63 percent in the year to Q3 compared to 60 percent one year earlier, driven by France over the year as a whole (with a very strong Q2 in particular) but more recently by the UK, (with a 42 percent increase in the past quarter). Germany by contrast has been slower in the past 2 quarters, starved of a sufficient supply of good quality property for sale in the more demanded markets.

At the same time, mounting demand, core supply shortages, increasing pricing and a search for yield are all still pushing investors towards new markets and demand in some areas has spiralled rapidly. Previously overlooked Western and Southern markets have benefited most but the same momentum is spreading to other areas such as Central Europe. Over the past year, it has been Ireland, Austria and the Netherlands which have been the three biggest winners in percentage terms but Spain is perhaps the standout recovery market, with its market share nearly trebling in the past 18 months (from 1.8 percent to 5.2 percent) and yields falling at a faster rate than in virtually any other market. Only Ireland in fact saw faster compression, with a 200bp drop in the past year compared to 130bp in Spain and 98 bp in Portugal.

Looking ahead, David Hutchings, Head of EMEA Investment Strategy at Cushman & Wakefield said: “We may have some weakness still in parts of the underlying consumer market around Europe but from an investment stance it’s a long time since the market has looked any stronger. We have more opportunities now emerging and an increasingly dynamic retailer market as changes in consumer trends and e-commerce filter through to how and where people are actually shopping. On top of this the ECB’s bank stress tests and emerging plans for quantitative easing will potentially add to both supply and demand and as a result, not only will we end 2014 on a high but all the signs point to no siesta for the markets in 2015.”

Łukasz Lorencki, senior surveyor at Cushman and Wakefield’s Capital Markets department in Warsaw, commented: “Unlike other European countries, the retail investment volume in Poland has fallen, seeing a 50 percent decline compared with the first three quarters of 2013 to the level of around €416 million. Despite this notable drop in the investment activity, investors continue to show strong interest in prime retail assets in Poland. The factor halting the investment activity is the dearth of supply of such assets. The only large-scale scheme that changed hands this year was CH Poznan City Center, while last year transactions involved the sale of Silesia City Center, Galeria Dominikańska and Złote Tarasy (the sale of Warsaw City Council’s shares in the centre). We predict that in Q4 as well as in the whole of 2015 the supply of large-scale facilities and retail portfolios will rise, which should be followed by an increase in the number of transactions.”