A staggering 1.88 million sqm of new shopping centre space has been developed across the European market in the first six months of 2014. Shopping centre development activity has largely remained concentrated in emerging markets, with a large proportion (84 percent) taking place in Central & Eastern Europe (CEE), according to the latest research from CBRE.

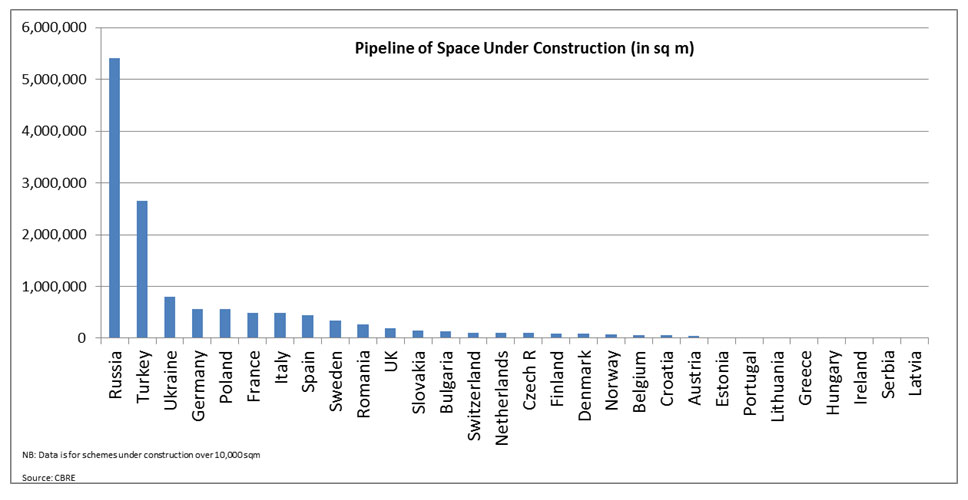

Across Europe, over 4.5 million sqm of shopping centre space opened in 2013 with Russia, Turkey, Poland and France seeing the greatest completion of space respectively. Russia and Turkey remain the most active markets, with over 60 percent of Europe’s shopping centre completions in 2013 located in these two countries. Russia has developed 1.5 million sqm of new stock in 2013. The development pipeline in Turkey continues to be notable with more than 2.6 million sqm of shopping centre space under construction in H1 2014. This high rate of construction is due to an improving economy and a continuing interest of developers in regional cities.

Other countries with notable shopping centre development in the pipeline include the Ukraine (793,759 sqm), Germany (564,275 sqm), Poland (559,586 sqm), France (491,971 sqm) and Italy (489,167). As has been the trend for several years, much of the activity is taking place in CEE but Germany saw a significant increase in shopping centre stock under construction in 2014, following the completion of the Sky Plaza in Frankfurt in 2013.

Natasha Patel, Associate Director, EMEA Retail Research, CBRE, commented: “Shopping centre development activity levels in Europe are similar to what they were last year in terms of location, with new construction dominated by CEE. In Turkey the majority of development, certainly the larger schemes, is taking place in the major cities such as Istanbul with smaller scheme development taking place in the outer regions such as Izmir in Turkey.”

She continued: “The scale of new development is largely to due to economic growth in the region, a growing middle class and the increasing demands of cross-border retailers, many of whom have found that the existing retail space in the region does not meet their requirements.”

Maxim Palt, Analyst, Research Department, CBRE in Russia, said: “The period of strong macroeconomic improvement, consumer income growth and lack of quality retail space during 2012-2013 resulted in a large volume of announced projects of shopping malls all over Russia. These projects not only cover cities where the population exceeds 500,000 inhabitants, but also smaller towns. The majority of these projects are in the last stages of development, hence new delivery of shopping malls in Russia as of 2014 could be 1.5 times higher than new delivery in 2013. The current geopolitical situation and its influence on the Russian economy will have downward pressure on new delivery of shopping malls in 2015. However, developers with small financial leverage have good opportunities to finalize their projects as consumer demand in the long run will remain high.”