JLL presents the Q1 2019 Moscow region warehouse market update. The vacancy rate has been declining for the past two years. According to JLL, the vacancy rate in the Moscow region warehouse market declined by 0.3 ppt in the first three months of 2019, to 4.2 percent. The take-up volume in Q1 2019 was 348,000 sqm, of which 60 percent transacted on the secondary market, in line with recent experience. Warehouse completions reached 132,000 sqm, almost double the level of Q1 2018.

“On the one hand, the positive quarterly dynamics of the main indicators is a signal of warehouse market recovery. On the other hand, there are a number of economic indicators, such as retail turnover, Purchasing Managers Index (PMI) and economic growth forecast which restrain optimism about the future market prospects,” commented Evgeniy Bumagin, Head of Industrial & Warehouse Department, JLL, Russia & CIS. “Major developers have actively started considering the purchase of land plots for industrial development in the Moscow region and they are ready to implement projects on demand. PNK Group has the largest number of new projects in Moscow region, among which there are PNK Park Veshki, PNK Park Pushkino, PNK Park Zhukovskiy. Furthermore, the developers, the Kholmogory company and Radius Group, announced the resumption of speculative construction and expansion of existing industrial parks.”

Notably, Q1 2019 new supply is dominated by speculative developments, among them are new buildings in PNK Park Valischevo (totally 31,000 sqm) and warehouse in Novoselki (28,000 sqm) by RCS Corporation. Only 60 percent of total Q1 2019 completions, or 75,000 sqm, was available on the open market.

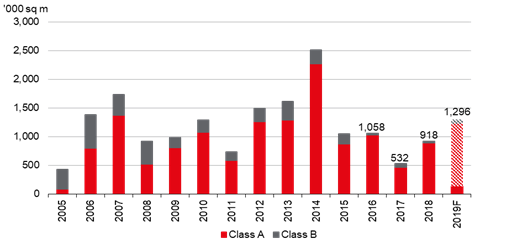

An additional 1.1 million sqm of new warehouse premises are scheduled for delivery until the year end. If the announced projects are delivered on time, the annual warehouse completions will be 1.4 times higher than those of 2018.

As in the previous year, a significant part of under construction projects (53 percent) were pre-leased at the stage of construction or had initially been built for end-users. The biggest projects of them are IKEA DC in Solnechnogorsk District (90,000 sqm), the second and third phases of Wildberries DC (50,000 sqm and 46,000 sqm) in the Koledino industrial park and a distribution centre for Lenta (70,000 sqm) in PNK Park Valischevo.

Among significant speculative projects announced for delivery in 2019 are the second phase of Sofyino industrial park (49,000 sqm) by Logopark Management company, a new phase in the warehouse complex Atlant Park (54,000 sqm) and a new building in LP Tomilino (24,000 sqm) by Tomilino Develoment company.

The total modern warehouse stock on the Moscow region warehouse market amounted to 17.9m sq m, of which 755,000 sq m is vacant space. “The available spaces are uneven in size, location and quality. For example, of 85 available blocks, 63 are small blocks of up to 10,000 sqm. As a result, they do not always meet demand requirements, at least in terms of the size, which leads to a sustained volume of vacant premises irrespective of the amount of deals on the secondary market,” explained Oksana Kopylova, Head of Retail and Warehouse Research, JLL, Russia & CIS.

According to JLL estimates, a few large speculative objects will be delivered to the market throughout the year, leading to an uptick in vacancy. If the demand stays high, we expect the vacancy rate to stabilize in the range of 4-5%.

The Q1 2019 take-up volume is comparable to the result of the previous quarter and the respective period of last year. The largest deal of the quarter is the purchase of PNK Park Koledino of over 53,000 sq m by Mistral Trading company (deal closed by JLL team). Among the landmark deals is the purchase of a new 50,000 sqm building in Vnukovo Logistics Center-2 by Russian Post.

In Q1 2019 retail has lost its leading position in the demand structure to logistic and manufacturing companies, and ranked third, with 21 percent of the transaction volume. Logistic and manufacturing companies showed high activity with 31 percent and 29 percent of the demand volume respectively. Nevertheless, taking into account the pipeline of future transactions, we expect retail to regain and strengthen its position in the next quarter.

The rental rates for new deals on the Moscow region warehouse market remain in the range of RUB3,600–3,800 per sqm per year (excluding VAT and operating expenses). A set of factors restraining and stimulating the growth of rental rates at the same time is becoming more noticeable.

“The selective growth of weighted average rental rates in particular projects were due to a sharp vacancy decline, from 8.3 percent to 4.5 percent YoY in 2018,” commented Evgeniy Bumagin. “Furthermore, the construction cost changes on the back of VAT increase and strengthening of labor and tax laws state monitoring were the factors behind rental rates growth.”

“On the other hand, there are barriers constraining rental rates growth. Primarily, moderate retail turnover growth; thus, the increase of demand by retailer sector is mainly driven by a process of consolidation,” added Oksana Kopylova. “Furthermore, pressure on rental rates comes from the high share of BTS-projects, 63 percent in 2018: existing buildings have to compete with the new schemes.”

All the above factors together with the positive market indicators allow JLL analysts to expect an increase of the average rental rates by 5-10 percent until the end of the year, depending on the direction and distance from MKAD.