International advisory company JLL has analysed how the direction of future retailer expansion in Poland relates to the supply of warehouse space. According to the summary, Eastern Poland, with the brightest prospect for retail supply growth, is suffering from a shortage of modern warehouse space.

The modern retail market continues to grow. According to JLL data, total retail stock is set to increase by 12 percent to 13.2 million sqm by the end of 2015. Currently, 44 percent of the existing space is located in the western and south-western regions, with an additional 17 percent in Central Poland.

It is the eastern part of the country that has seen the strongest growth (average 27 percent) in modern retail stock. New completions will include both large projects (such as the newly-opened Atrium Felicity in Lublin or Galeria Warmińska in Olsztyn) as well as numerous smaller schemes. In the East, the first outlet centres will also be delivered (in Lublin and Białystok).

Anna Bartoszewicz-Wnuk, Head of Research and Consultancy Poland, JLL, commented: “Along with the growth in the purchasing power and improvements to the road infrastructure in the East, developers and retail chains are keen to expand in this area of Poland. This interest is markedly bolstered by the influx of shoppers from across the eastern border, additionally reinforced by a local border traffic agreement with the Kaliningrad region.”

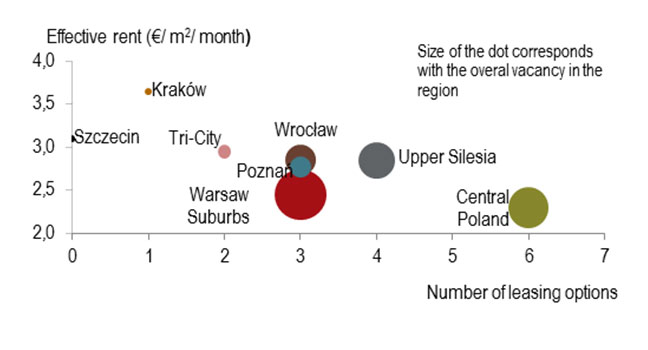

Although the eastern part of the country will witness the strongest percentage growth in retail stock, it is still worth remembering that retail stock in this region is significantly lower than in central and south-western parts of Poland. The development of retail chains in Eastern Poland may result in higher demand for warehouse space. However, with the region’s modern stock continuing to lag behind, the gap between supply and demand looks set to widen. Total modern warehouse stock for lease currently stands at 7.5 million sqm, 92 percent of which is located in 5 regions (Warsaw, Upper Silesia, Poznań, Central Poland and Wroclaw).

Tomasz Mika, Head of Industrial Agency Poland, JLL, said: “Retail chains make up the 2nd, after logistic operators, largest group, with a 24 percent share in demand for logistic space in the last 5 years. The average size of a unit leased by such a company is around 10,000 sqm. The best availability of this kind of units can be observed in Central Poland and Upper Silesia. In other parts of Poland the selection of such space for immediate lease is limited. An alternative to the already existing assets is tailor-made BTS projects. Due to the extended period of such an investment development, the decision to start cooperation with a developer should be made in advance.”