According to AXI IMMO’s latest summary on the current trends in Poland’s industrial market after the first half of 2015, good macroeconomic results are positively stimulating the development of the warehouse and production sector in Poland.

Strong demand at a level of 1.27 million sqm and falling vacancy rates in all regions are motivating developers to start new investments not only in mature markets, but also in new locations. 680,000 sqm of modern industrial space is currently under construction, of which speculative investments account for 172,000 sqm. Another 100,000 sqm is at the building permit stage.

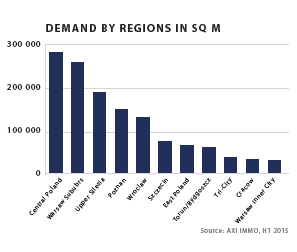

At the end of June, gross demand, i.e. new contracts, expansions and extensions, amounted to 1,270,000 sqm and was about 350,000 sqm higher than in the same period in 2014. 63 percent of transactions were new leases and expansions of clients’ existing locations. The most amount of space, 270,000 sqm, was leased in the region of Central Poland and in Warsaw. The highest net demand, 164,000 sqm was also recorded in Central Poland, followed by the Poznan region and Upper Silesia. Apart from the main regions, there was a visible increase in demand in new markets such as Lublin and Rzeszów, where a total of more than 100,000 sqm was leased.

“The current economic growth is based on fundamentals that are more robust than in previous cycles. Inflation remains low, and we have observed reasonable growth in credit and a declining deficit in the current account, as well as stable growth in private consumption, which is indirectly affecting the rapid development of the industrial property market in Poland,” said Renata Osiecka, Managing Partner at AXI IMMO. “The large portion of new demand is generated by companies from the end consumer market. We estimate that at the end of the year, net demand may be similar to last year’s record and exceed 1.4 million sqm.”

In the structure of demand in the first half of the year, logistics operators as usual had the largest share (33 percent), but it is worth noting that companies from the home&interior and electronics sectors had a higher share than in previous years, with 17 percent and 13 percent respectively of total demand recorded.

In the first half of the year, 472,000 sqm were completed. This is an increase in supply by 58 percent compared to the same period last year. The largest share of which was, 182,000 sqm in the Poznan region within five developments.

“We have observed a high level of activity among developers, with more than 680,000 sqm of modern warehouse space under construction, of which over 170,000 sqm is speculative space. Compared with the same period last year, the volume of speculative space realized is over two times as high. In addition it is worth to mention that beside the large number of projects under construction, developers are acquiring secured land for new investments in almost every market. This applies to mature markets such as Warsaw or Poznan, but also new locations such as Bydgoszcz and Lublin,” added Renata Osiecka.

At the end of the second quarter 2015, the vacancy rate was 5 percent. This is a decrease of 0.7 percent from the first quarter of this year. In annual terms it has fallen by 5.4 percent, and historically it is now at its lowest average rate. 480,000 sqm are currently available for lease. Availability in all regions has fallen below 10 percent. The highest amount of free units remain in Warsaw (9.7 percent) and the surrounding region (9.5 percent), followed by Upper Silesia. The lowest vacancy rates, below 3 percent, are in Poznan and Wroclaw. It should also be noted that part of the space is occupied under short-term contracts, and is not therefore formally counted as leased space.

In the last six months rents have remained stable. In subsequent quarters in most markets, transaction rates should remain unchanged, despite the low level of vacant space. AXI IMMO expects some small increases in Central Poland due to the low availability of space and the lack of speculative investments.

In the second half of the year AXI IMMO expects the high level of development activity to remain unchanged. The low vacancy rate will encourage developers to start new investments, and it is possible that some of them will be speculative projects – mainly in the Warsaw region as well as in new locations after signing pre-let agreements.

In terms of demand, the growth trend should continue, mainly through the development of companies already present in the Polish market. The sectors with the greatest potential for growth remain FMCG, electronics and home&interior particularly in the e-commerce sales channel.

At current demand and supply growth, especially growth in speculative projects, the vacancy rate should remain stable. Rents are stable with a slight upward trend in selected locations.